Risk-specialised AI is already giving early adopters week, sometimes months of lead time on credit deterioration that used to arrive as quarterly surprises. The banks using it aren't waiting for the next filing. They're acting before the problem reaches the books. The question isn't whether AI can solve this. It's whether your institution is using it or still relying on tools built for a world that no longer exists.

Banks today face a simple reality: Geopolitical risk is no longer a remote tail risk, but a constant stress on lending portfolios. Major conflicts and trade disruptions: from the Eastern European war to new international trade standards and the recent ongoing conflict in the Middle East, have already reshaped credit conditions. And most banks' monitoring infrastructure wasn't built to see any of it in time.

In fact, a recent EY survey finds that 95% of CROs in Europe and 90% in the Middle East/North Africa say geopolitical developments are driving their strategic agendas. Meanwhile, 62% of banks rank credit risk as a top concern again, and the awareness is growing.

Yet most banks’ monitoring frameworks still rely on slow, periodic reviews. Quarterly portfolio reports and annual credit reviews assume a stable world. Today’s crises unfold in weeks, not years. By the time a conflict-driven stress appears in financial filings, the hit is often already in the books. Banks need to ask: Can our existing monitoring truly see these risks before they become losses?

The core problem isn't awareness — most credit teams know geopolitical risk is real. It's that the standard monitoring toolkit wasn't designed for this kind of risk. Traditional credit monitoring looks at balance sheets and past financials. Annual reviews, sector-level stress tests, static concentration limits, these were built for a world where risks were periodic, their transmission mechanisms were understood, and you had time to respond. That world has gone. And the data that would reveal today's risks exists; it's just not in the places conventional tools look.

Geopolitical exposure rarely appears as a line item. Consider these examples:

A project finance facility for a UAE petrochemical plant doesn't flag its Strait of Hormuz vulnerability.

A trade credit line to a Ukrainian grain exporter doesn't mention Black Sea shipping.

An SME facility in Turkey doesn't surface its exposure to regional demand collapse next door. The risk is embedded across the portfolio — it just doesn't surface in conventional monitoring until it's become a provisioning event.

Risk-specialised AI can surface all three. By mapping supply chain dependencies, revenue geographies, and funding structures against live geopolitical signals — continuously, at portfolio scale — it connects the dots that static reports miss until they've become provisioning events.

The indirect transmission makes this harder still. A bank with no loans in the Middle East can still suffer from Gulf turmoil via higher oil prices or regional contagion. Roughly 15–20 million barrels per day (20% of global oil supply) flow through the Strait of Hormuz. Around 12% of all global trade passes through the Red Sea/Suez Canal — recent attacks there forced carriers to reroute around Africa, adding nearly two weeks to transit times, with insurance premiums spiking 50%+ on war-risk cover.

As Moody's notes, geopolitical fracturing can spill swiftly into credit markets via risk premia and funding stress — often several counterparties removed from the original event. Only institutions continuously monitoring non-financial signals will catch these hidden exposures in time. Conventional tools, by design, cannot.

Region/Conflict | Primary Credit Channel | Risk Level | |

|---|---|---|---|

Middle East/Gulf Conflict: Strait of Hormuz | Oil price shock → import inflation → corporate margin compression; energy sector NPLs; sovereign CAD widening | Critical | |

Eastern Europe Conflict | Trade finance disruption; energy supply re-routing; FX volatility; sovereign debt stress across CE/Balkans | Critical | |

South/Southeast Asia: Tariff shock, supply chain | Manufacturing investment slowdown; EM currency volatility; NBFI credit quality; export sector stress | High | |

Latin America/MENA: Rising sovereign debt gearing | Higher net-debt-to-sales ratios; governments reliant on banking sectors for local currency funding | Elevated | |

Region/Conflict | Primary Credit Channel | Risk Level | |

|---|---|---|---|

Middle East/Gulf Conflict: Strait of Hormuz | Oil price shock → import inflation → corporate margin compression; energy sector NPLs; sovereign CAD widening | Critical | |

Eastern Europe Conflict | Trade finance disruption; energy supply re-routing; FX volatility; sovereign debt stress across CE/Balkans | Critical | |

South/Southeast Asia: Tariff shock, supply chain | Manufacturing investment slowdown; EM currency volatility; NBFI credit quality; export sector stress | High | |

Latin America/MENA: Rising sovereign debt gearing | Higher net-debt-to-sales ratios; governments reliant on banking sectors for local currency funding | Elevated | |

“Geopolitical risk needs to be managed as a cross-cutting driver. It can affect banks through multiple channels — financial markets, the real economy, and the safety and security of operations. Its impact cuts across credit, market, liquidity, business model, governance and operational risks.”

— European Central Bank Banking Supervision, November 2025

Many banks are already experimenting with AI, deploying general-purpose tools on financial filings, asking them to summarise annual reports or flag sector themes. The results feel useful. But they mask a critical problem.

General-purpose AI was not built for credit risk. It can read a 10-K/annual reports and produce a plausible summary, but it cannot tell you that a borrower's revenue is 60% concentrated in a sanctioned corridor, or that their Days Sales Outstanding (DSO) has deteriorated 40% quarter-on-quarter while their revolving credit facility approaches its limit.

The critical distinction is not whether you are using AI. It is whether the AI you are using was built for credit risk or simply adapted from a general-purpose model that happens to be good at language.

Capability | Generic AI (ChatGPT / General LLMs) | Risk-Specialised AI (e.g. CreditX by Galytix) | |

|---|---|---|---|

| Training domain | General internet content; broad but shallow on credit risk nuance | Trained on credit data: financials, covenants, defaults, EM recovery rates, geopolitical indices |

| Financial statement analysis | Summarises; misses covenant breaches, off-balance sheet exposure, segment-level flags | Automatically spreads financials, detects anomalies, flags covenant risks and related-party links |

| Geopolitical signal integration | Provides generic commentary; no portfolio linkage | Maps live signals (CDS, FX, shipping) directly to specific positions in the book |

| Time to insight (per borrower) | Hours of manual analyst work to prompt, verify, and interpret | Minutes — with full source attribution, no black-box outputs |

| Auditability / Governance | Outputs not linked to source data; difficult to defend in regulatory review | Every flag links back to the underlying data point; audit trail built-in |

| Portfolio-level view | Single borrower at a time; no aggregation across book | Portfolio-wide screening, sector-geography intersection analysis, concentration limits in real time |

| Early warning lead time | Reactive to news available to anyone | Weeks to months ahead of financials via non-financial signals |

| Typical productivity gain | Limited — still requires significant analyst re-work to validate | 40%+ reduction in credit review cycle time; 20–30 hours of analysis compressed to minutes |

Capability | Generic AI (ChatGPT / General LLMs) | Risk-Specialised AI (e.g. CreditX by Galytix) |

|---|---|---|

Training | General internet content; broad but shallow on credit risk nuance | Trained on credit data: financials, covenants, defaults, EM recovery rates, geopolitical indices |

Financial statement analysis | Summarises; misses covenant breaches, off-balance sheet exposure, segment-level flags | Automatically spreads financials, detects anomalies, flags covenant risks and related-party links |

Geopolitical signal integration | Provides generic commentary; no portfolio linkage | Maps live signals (CDS, FX, shipping) directly to specific positions in the book |

Time to insight (per borrower) | Hours of manual analyst work to prompt, verify, and interpret | Minutes — with full source attribution, no black-box outputs |

Auditability / Governance | Outputs not linked to source data; difficult to defend in regulatory review | Every flag links back to the underlying data point; audit trail built-in |

Portfolio-level view | Single borrower at a time; no aggregation across book | Portfolio-wide screening, sector-geography intersection analysis, concentration limits in real time |

Early warning lead time | Reactive to news available to anyone | Weeks to months ahead of financials via non-financial signals |

Typical productivity gain | Limited — still requires significant analyst re-work to validate | 40%+ reduction in credit review cycle time; 20–30 hours of analysis compressed to minutes |

The productivity difference is stark. Tasks that once required a team 20–30 hours of manual analysis — spreading financials, reading filings, checking related-party links, mapping supply chain geographies can be compressed to minutes with risk-specialised AI. That's not marginal efficiency. That's a structural change in how many credits a team can actively monitor, and how far ahead of problems they can operate.

Why Generic AI Falls Short | What Risk-Specialised AI Delivers |

|---|---|

Generic LLMs were not trained on credit risk data. They can read a 10-K/10-Q/Annual Reports and produce a plausible summary — but they cannot tell you that a borrower's revenue is 60% concentrated in a sanctioned corridor, or that their Days Sales Outstanding has deteriorated 40% quarter-on-quarter while their revolving credit facility approaches its limit. | Purpose-built credit AI is trained on decades of EM loan data — defaults, recoveries, sector-specific stress patterns — and integrates live geopolitical signals directly against portfolio positions. Every output is traceable to the underlying source data. This enables consistent interpretation of borrower health across markets, surfacing concentration risks, early warning signals, and structural vulnerabilities that generic systems fail to contextualise or prioritise. |

Why Generic AI Falls Short |

|---|

Generic LLMs were not trained on credit risk data. They can read a 10-K/10-Q/Annual Reports and produce a plausible summary — but they cannot tell you that a borrower's revenue is 60% concentrated in a sanctioned corridor, or that their Days Sales Outstanding has deteriorated 40% quarter-on-quarter while their revolving credit facility approaches its limit. |

What Risk-Specialised AI Delivers |

|---|

Purpose-built credit AI is trained on decades of EM loan data — defaults, recoveries, sector-specific stress patterns — and integrates live geopolitical signals directly against portfolio positions. Every output is traceable to the underlying source data. This enables consistent interpretation of borrower health across markets, surfacing concentration risks, early warning signals, and structural vulnerabilities that generic systems fail to contextualise or prioritise. |

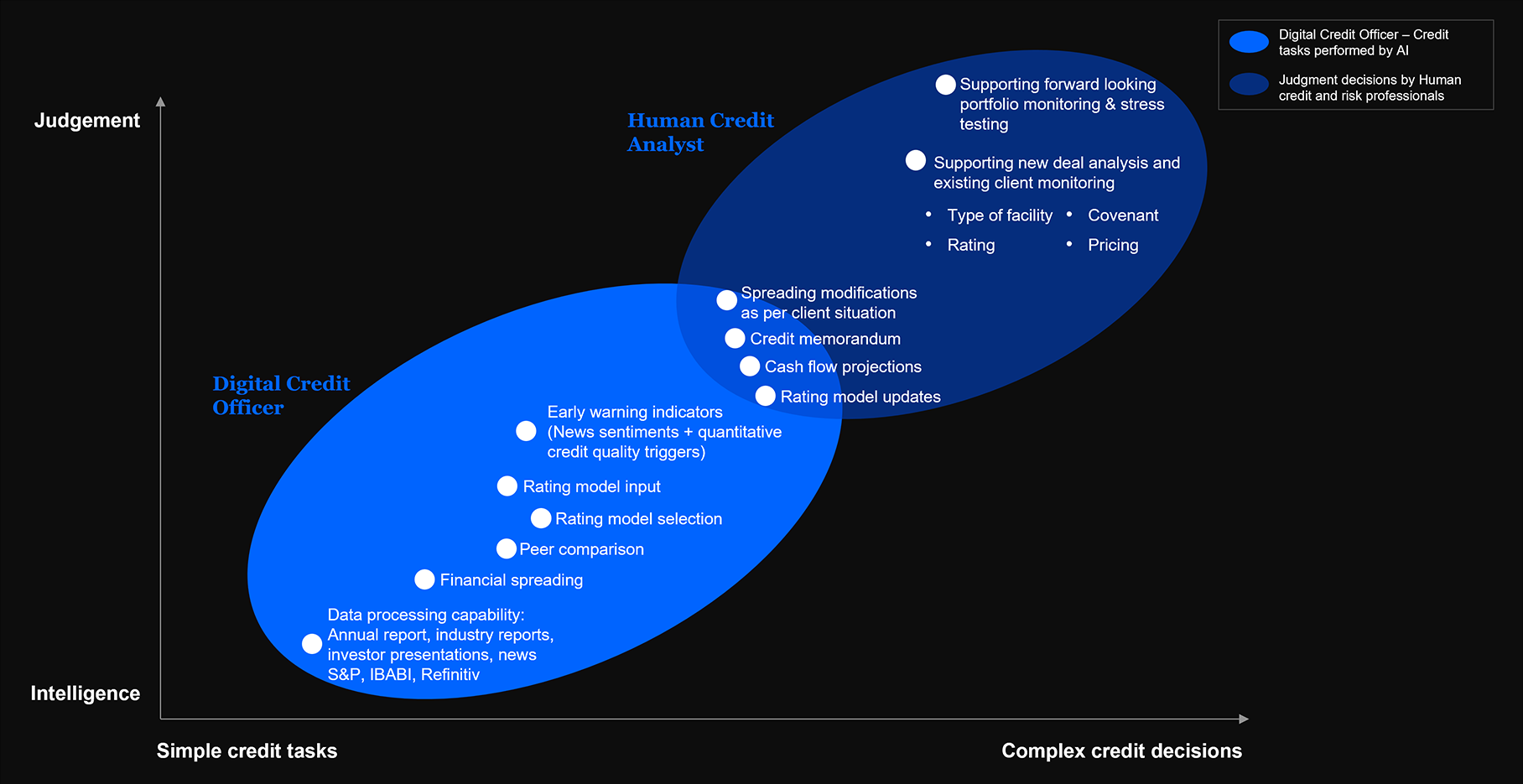

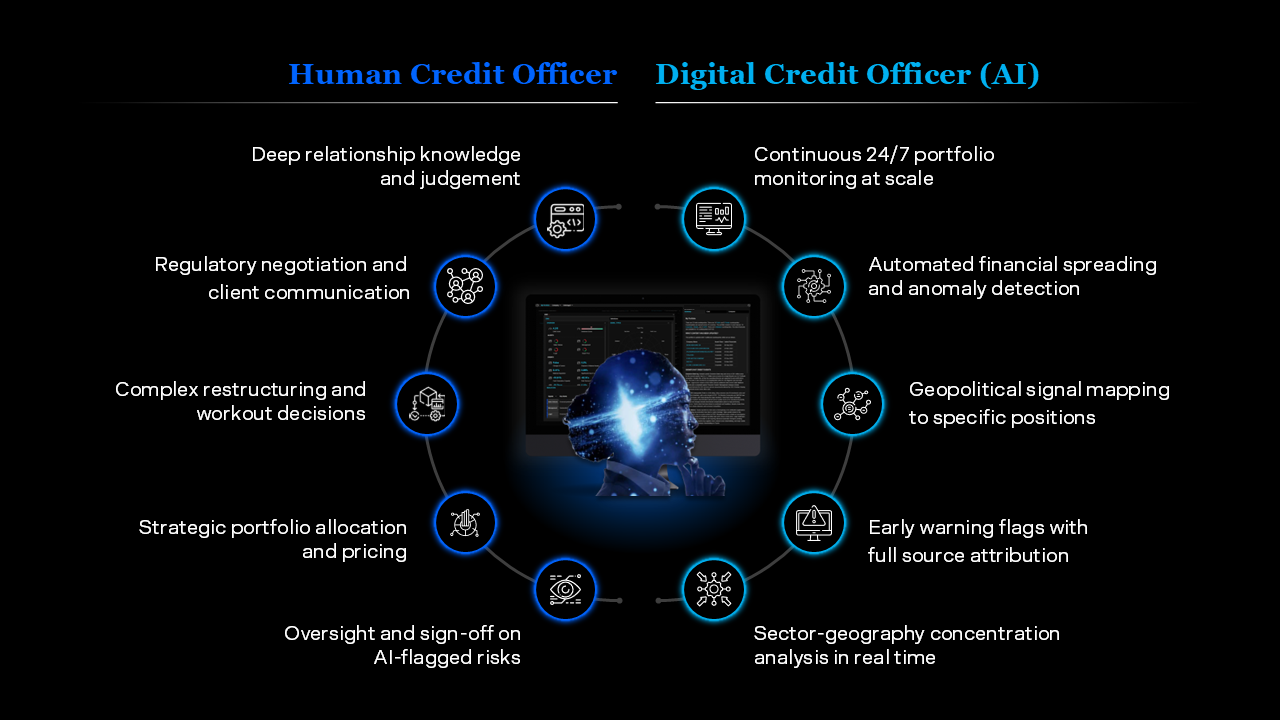

The most effective AI deployment model in credit risk is not AI replacing analysts. It's the Digital Credit Officer — an AI system that works continuously alongside human counterparts, handling the volume and velocity of data processing that no human team can match, and surfacing the judgement calls that require experienced credit professionals.

As illustrated above, the Digital Credit Officer operates across simple, high-volume credit tasks at scale — financial spreading, peer comparison, early warning indicators, rating model inputs — while the Human Credit Analyst retains full ownership of complex, judgement-intensive decisions. The overlap zone, from credit memoranda to portfolio stress testing, is where the two work most powerfully in tandem.

What the Digital Credit Officer does in practice:

Automatically reads all borrower financials and segment notes — detecting growing revenue concentration in sanctioned corridors, covenant proximity, deteriorating liquidity metrics — and flags the credit memo for human review before the next quarterly cycle.

Monitors portfolio-wide sector-geography intersections in real time — surfacing compounding risks in EM books that static systems miss entirely.

Streams non-financial early warning signals — sovereign CDS spreads, shipping volumes, FX moves, trade flow data — directly to the positions in the book they affect, giving credit teams lead time to act.

CROs and risk teams should take concrete steps today to transform credit and portfolio management for the AI era:

Embed Continuous Monitoring: Move beyond annual or quarterly cycles. Ensure that portfolio dashboards update in real time with new data (market moves, shipping alerts, rating changes).

Map Hidden Exposures: Commission data exercises to chart actual revenue and supply-chain links for key borrowers. Use data providers or AI to augment manual risk rating narratives.

Stress-Test Tail Scenarios: Regularly run stress tests with scenarios like extended oil price shocks, supply-chain closures, or mass cyber disruptions. Allocate capital or limits based on these scenario outcomes.

Replace Generic AI with Risk-Specialised Analytics. Build or procure AI models trained on credit risk data such as financials, covenants, EM recovery rates, geopolitical indices. Insist on transparency: every model output must link back to source data, not black-box guesses.

Deploy the Digital Credit Officer Alongside Your Team. The goal is not to automate credit decisions, it is to give your human credit officers the data, signals, and lead time they need to make better ones. Measure the ROI: 40%+ cycle time reduction is achievable in the first year of deployment.

In the new era, visibility is protection. The banks that succeed will not be those who got lucky with geography or timing. They will be the ones who built the capability to see their exposures clearly and early and who gave their credit teams the tools to act on that visibility.

The good news: the technology exists today. Risk-focused specialised AI can now stream financial statements, news, market signals, and geopolitical indices into a unified risk view automatically alerting credit teams when a borrower's profile shifts in ways that matter. Early adopters report actionable warnings weeks or even months ahead of what traditional reviews would catch.

The question is no longer whether to invest in AI-powered credit monitoring. It's how quickly you can build the capability and how much it's costing you not to.

Monitor Your EM Exposure in the New Geopolitical Era.

CreditX from Galytix gives credit teams a continuous, portfolio-wide view of geopolitical exposure, counterparty risk, and early warning signals — before they reach a filing. Live with risk professionals across 30+ banks in 52 countries.